Actionable Energy Sector Idea

Actionable Energy Sector Idea

Part II of our, "Energy Won't Always Go Up" note.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Gravity Always Wins?

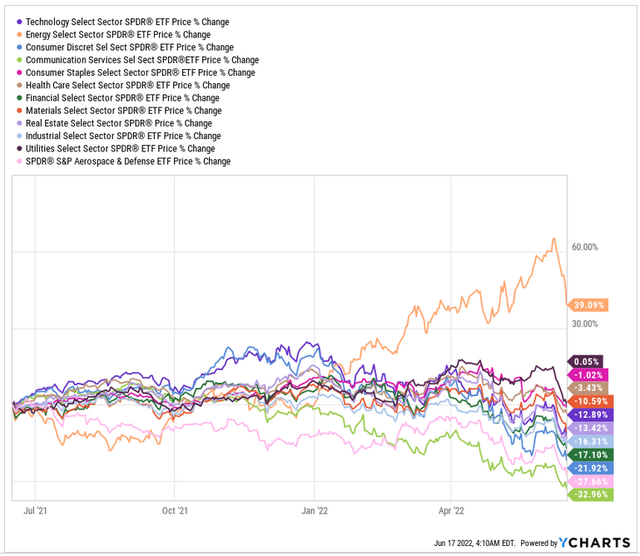

In the last twelve months, the only sector to have generated positive gains is energy. That is a remarkable statement. It's common to find that value or growth has been the outperformer, that a cluster of sectors - say, tech & healthcare & financials - have done well whereas others - say defense, utilities and energy - have not. It's not common to find only one sector in positive territory for a whole year.

Probably it was not intended to be that way. A year back when energy was looking all beaten up we imagine that large institutions were accumulating stakes in anticipation of a run-up in the sector. But the ongoing supply chain problems that persist post Covid helped more than might have been expected; if you can't transport fuel products as easily as was once the case, those products will become scarce in key demand areas and prices will rise, to the benefit of companies in the sector. The Russian invasion of Ukraine was then a gift; the further reduction in supply coupled with sanctions leading to two drivers of higher prices were a doozy for the sector.

This is what has happened in the last 12 months, using SPDR sector ETFs as a proxy.

Only energy is up; utilities flat; everything else down. Diversification has been a bust. Either you were long energy and/or short growth, or your year has been tough.

For a couple weeks now in our premium Growth Investor Pro service we've been saying, energy looks like it is going to correct - and as you can see from the chart above, that trend has started. We believe it can continue. The reason we believe it can continue is nothing to do with the real world, although we do believe that any suspension or cessation of the Russian invasion of Ukraine can lead to an increase in supply which ought itself to drop prices and drop sentiment in the sector. No, we believe that sector rotation alone can cause energy to drop down and the other sectors to move up.

Energy represents a tiny component of the major indices - around 3.5% of the Dow, 4.8% of the S&P, and a negligible proportion of the Nasdaq-100.

If large investors sell energy stocks, they have to put that money somewhere. Most likely in our view it gets invested in the most beaten-up sectors - just as was happening to energy itself a year or more ago. If capital moves out of energy and into any of the more meaningful proportions of the major indices - that means tech, healthcare, financials, consumer - then we would expect that to be bullish for the indices.

In our other work as you know we are bullish on the indices and on the better quality single-stock tech names. We don't therefore propose any kind of fancy pair trade, it's not necessary in our view since we have plenty of long ideas and indeed long positions in staff personal accounts.

We do think that short energy can work, and this is our idea. It’s for paying subscribers only - if you want to join us, you can subscribe right here for only $19/mo or $149/yr.